Benefit In Kind Malaysia Tax

Chapter 4 B Employment Income

Guide To Filing Taxes In Malaysia Defining The Benefits In Kind In Form Ea

Individual Income Tax In Malaysia For Expatriates

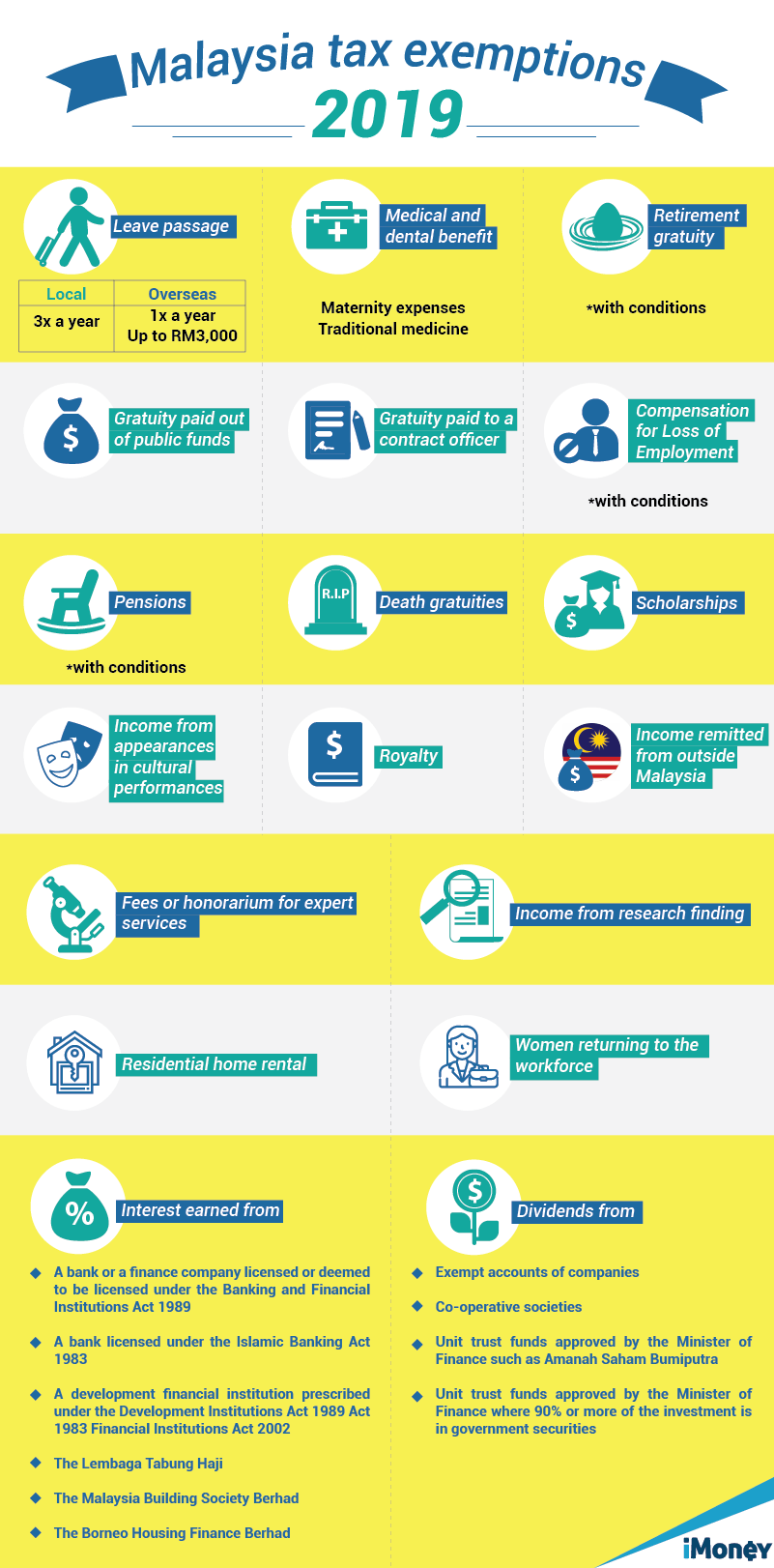

Get More Tax Exemptions For Income Tax In Malaysia Imoney

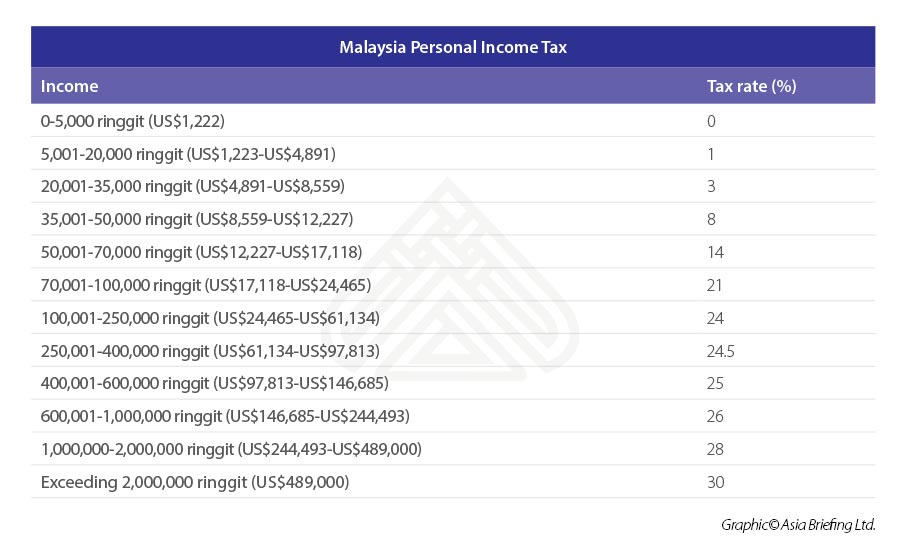

Malaysia Personal Income Tax Guide 2017

Employment Income

12 december 2019 page 1 of 27 1.

Benefit in kind malaysia tax. Objective the objective of this ruling is to explain a the tax treatment in relation to benefit in kind bik received by an employee from his employer for exercising an employment and. Employers goods provided free or at a discount. Objective the objective of this public ruling pr is to explain a the tax treatment in relation to benefit in kind bik received by an employee from his employer for exercising an employment and. 19 november 2019 4 2 perquisites are benefits in cash or in kind which are convertible into money received by an employee from his employer or from third parties in respect of having or exercising an employment.

These benefits are normally part of your taxable income except for tax exempt benefits which will not be part of your taxable income. When taxable biks must be added to the payroll so they can be included in the pcb calculation. Inland revenue board of malaysia benefits in kind public ruling no. 11 2019 date of publication.

Benefits in kind biks are benefits provided to the employee by or on behalf of the employer that cannot be converted into money. Benefits in kind are benefits provided by or on behalf of your employer that cannot be converted into money. 2 2 however there are certain benefits in kind which are either exempted from tax or are regarded as not taxable. Inland revenue board of malaysia date of publication.

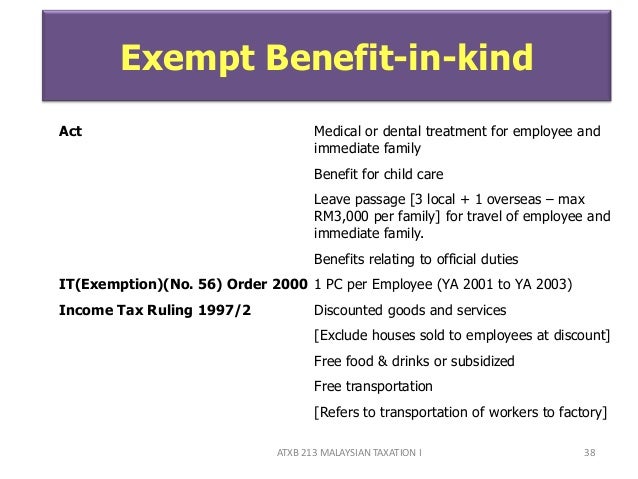

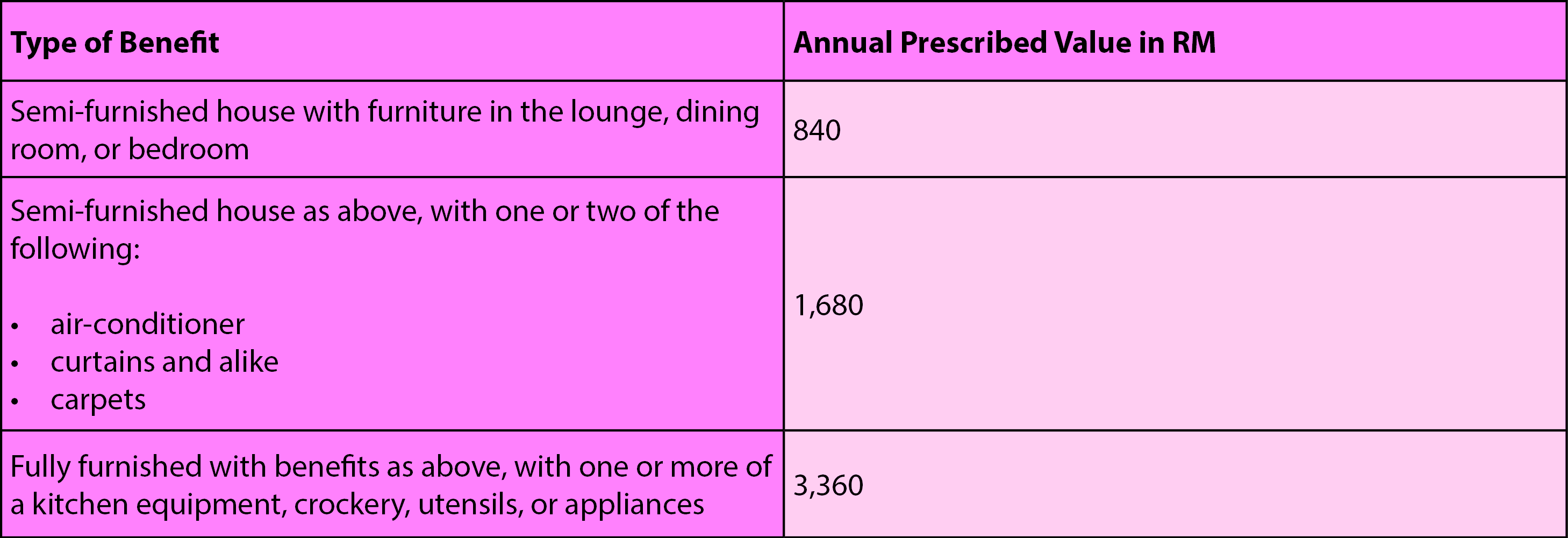

Any benefit exceeding rm1 000 will be subject to tax. Perquisites are taxable under paragraph. These benefits are called benefits in kind bik. 3 2013 date of issue.

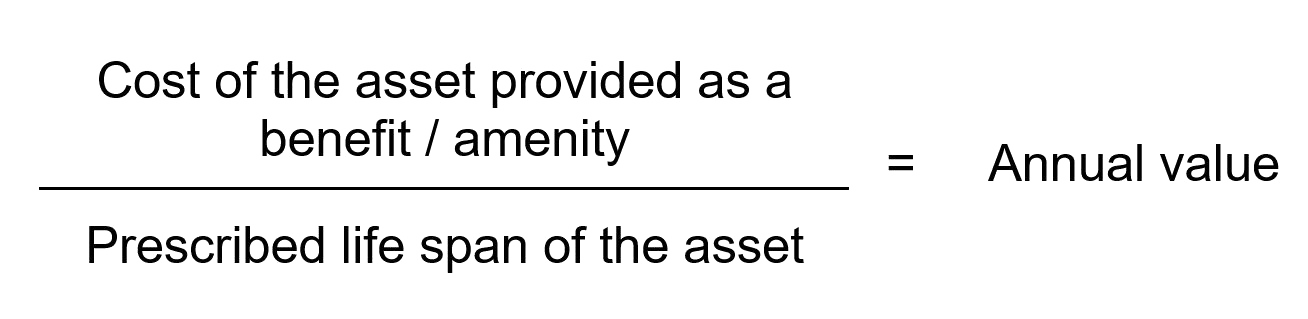

Tax exemption on benefits in kind received by an employee 2 1 benefits in kind received by an employee pursuant to his employment are chargeable to tax as part of gross income from employment under paragraph 13 1 b of the income tax act 1967 ita. Generally non cash benefits e g. There are several tax rules governing how these benefits are valued and reported for tax purposes. Inland revenue board of malaysia benefits in kind public ruling no.

One overseas leave passage up to a maximum of rm3 000 for fares only. 15 march 2013 pages 1 of 31 1. Accommodation or motorcars provided by employers to their employees are treated as income of the employees. And one should also be awar.

Exemption is available up to rm1 000 per annum. 3 local leave passages including fares meals and accommodation.

Benefit In Kind Liberal Dictionary

Malaysian Bonus Tax Calculations Mypf My

Benefits In Kind Bik

Smeinfo Understanding Tax

Tax Exemptions What Part Of Your Income Is Taxable

5 Key Facts You Probably Didn T Know About Tax Deductibles In Malaysia

Https Www2 Deloitte Com Content Dam Deloitte Global Documents Tax Dttl Tax Malaysiahighlights 2020 Pdf

Malaysia Payroll And Tax Information And Resources Activpayroll

Https Www2 Deloitte Com Content Dam Deloitte My Documents Tax My Tax Employers Mandate Talentcorp 13082015 Jb Slides 2 Noexp Pdf

Esos What You Need To Declare When Filing Your Income Tax

Malaysia Tax Relief Stimulus Measures For Individuals Kpmg Global

Personal Income Tax Guide For Expatriates Working In Malaysia

Https Www Pwc Com My En Assets Publications 2018 2019 Malaysian Tax Booklet Updated Pdf

Individual Life Insurance Vs Group Term Life Insurance Fbs Life Insurance Quotes Term Life Life Insurance Types

Corporate Tax Malaysia 2020 For Smes Comprehensive Guide Biztory Cloud Accounting

Gst Accounting Software Malaysia Best Accounting Software Accounting Software Accounting

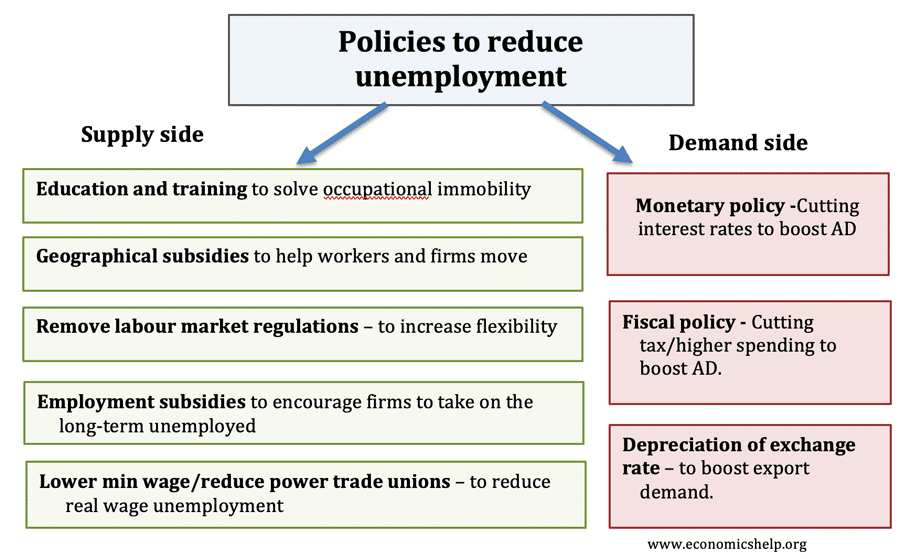

Policies For Reducing Unemployment Economics Help

Gst Is The Single Indirect Tax That Is Levied On The Supply Of Goods And Services Between Different Entit Indirect Tax Goods And Service Tax Goods And Services

Https Encrypted Tbn0 Gstatic Com Images Q Tbn 3aand9gcqdz8yfhjaf6 Srpsalkwejj7wnpwwu Lq54xrpmhecp H0zf4s Usqp Cau

A Notice Of Assessment Or Noa Is A Statement From The Canada Revenue Agency Notifying The Taxpayer Of The Amount Of Tax They Assessment Tax Credits Income Tax

Personal Income Tax E Filing For First Timers In Malaysia Mypf My

Should You Invest In Sspn Mypf My

What Is The Malaysian Tax For Foreign Owned Companies